OTW #56: Beginner's guide to options, Bank fears again, (Un)affordable cities, and more.

OTW #56: Beginner's guide to options, Bank fears again, (Un)affordable cities, and more.

Important financial stories to check out over the weekend

It’s time for “Over the Weekend.” If you enjoy these weekly 5-minute posts, please

share The Antagonist with others. When your referrals subscribe, you’ll receive credits toward a free premium membership.

hit the heart button at the bottom of this post. Doing so helps improve The Antagonist’s visibility on Substack.

1. What are stock options? A beginner’s guide.

One common myth is that holding stocks for years is the only way to succeed in the market. While this is a profitable strategy, there are other ways to reach your financial goals too.

One of the most powerful — and most misunderstood — strategies is stock options.

With options, you can achieve returns much higher than a simple buy-and-hold strategy. You also don’t have to wait until retirement to realize your profits.

Nearly everything you’ve heard about options is false

Options have a bad reputation. Most people see them as too risky or too advanced for everyday investors.

Neither are true.

I admit that at first glance, options are confusing. They have their own vernacular, and broker platforms look like spreadsheets hopped up on a dozen espressos. Like most things, however, once you learn the basics, options become fairly simple.

If you understand how to trade stocks, you can understand options.

I believe that the mystique surrounding options is intentional. As long as Wall Street can convince you that options trading is best left to professional money managers, they can keep charging exorbitant fees.

That’s why I wrote “What are Stock Options? A Beginner's Guide.” My goal is to demystify options trading for you.

The article isn’t simply theoretical knowledge either. I give you practical tools to unlock new possibilities in your investment journey.

If this sounds interesting to you, check out the full article here.

2. Wait…wasn’t the bank crisis behind us?

Less than a year ago, the Fed tried to convince us that the regional bank crisis was over. This data from The Kobeissi Letter suggests otherwise:

US Regional Bank Stocks 1 Month Into 2024:

NY Community Bank, NYCB: -60%

Valley National Bank, VLY: -25%

Metropolitan Bank, MCB: -15%

HarborOne, HONE: -14%

Comerica Bank, CMA: -13%

Zions Bank, ZION: -12%

Western Alliance, WAL: -11%

Citizens Financial, CFG : -6%

KeyCorp, KEY: -5%

Regional bank worries resurfaced as New York Community bank, which acquired the collapsed Signature Bank, cut their dividend by 70%.

These are the same banks that hold nearly 70% of commercial real estate loans.

New York Community Bank is [also] one of the largest mortgage originators in the US. They currently have over $100 billion in assets.

Antagonist’s take

The regional banking problem spans much wider than the stock market. When First Republic Bank collapsed last year, JPMorgan (JPM) acquired most of its assets in a government auction.

That situation was rife with questions, and it resurfaced the too-big-to-fail concerns that arose out of the 2008 financial crisis. By many accounts, it appeared that JPM got a sweetheart of a deal because of its preferred status with the federal government.

It’s true that large, well-capitalized banks can enhance a country’s competitiveness on the international stage. But consolidation into already-behemoth institutions like JPM also increases the risk of the failure of a single entity threatening the stability of the entire financial system.

Consolidation also puts pressure on smaller, community banks, which often serve unique local markets. They can easily get squeezed out, however, as too-big-to-fail banks get even bigger.

I’m already uneasy about power being concentrated among a select few. When this power is held by banks that have a favored status with the federal government, my uneasiness turns into outright skepticism.

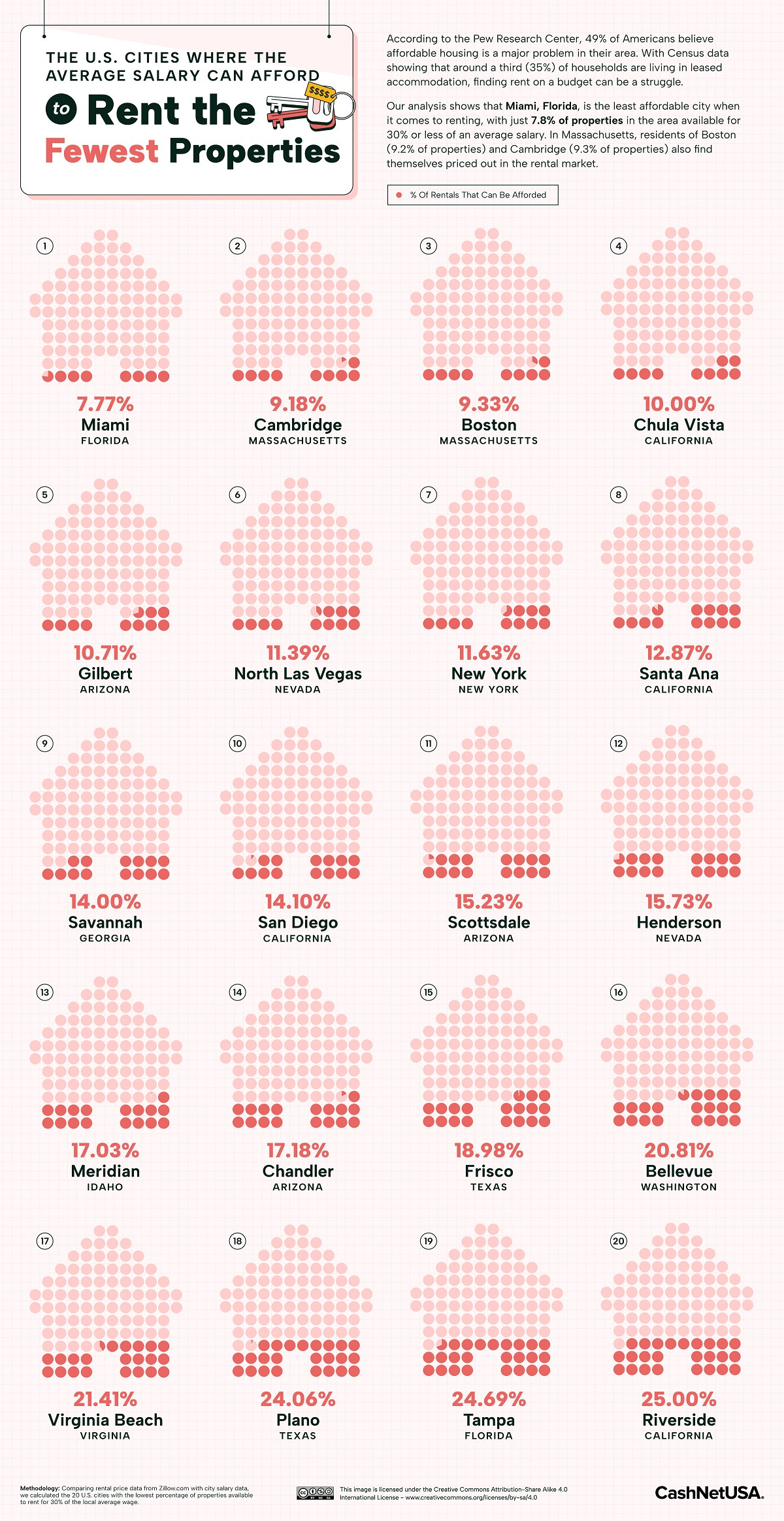

3. Housing: most/least affordable cities to rent in and the biggest bubble risks.

Visual Capitalist just ran a series on the housing market. They analyzed the most and least affordable U.S. cities to rent in on an average salary:

Most affordable U.S. cities for rent on an average salary.

Least affordable U.S. cities for rent on an average salary.

Antagonist’s take

Despite all the Fed’s talk about fighting inflation, nothing matters much if we can’t get housing and utilities costs under control. Those items comprise a significant portion of consumer spending.

Renters aren’t the only ones feeling trapped either.

Rising interest rates have only compounded the problem of limited supply in the housing market. Homeowners sitting on a 3% mortgage are understandably reluctant to sell their homes right now. If they did, they’d likely have to take on a loan with double the interest rate (or more) than they’re currently paying.

That doesn’t mean, however, that the housing market can’t crash. Visual Capitalist also compiled this list of the global cities with the highest real estate bubble risk.

Free trial reminder.

If you sign up before the end of this month, you can get a premium membership free for 30 days. This gives you access to trade alerts, the Challenge Portfolio, and the Blend Portfolio. Cancel any time.

Last thing...

To limit the length of Over the Weekend to 5 minutes, I can only highlight a few stories.

If you’d like to receive more summaries and links to important events and data,

Follow my personal X (Twitter) account and The Antagonist.

Thank you for reading, and have a great weekend!

Jason Milton

X (formerly Twitter) | LinkedIn | Facebook | Instagram | Medium

P.S. If you enjoyed this edition of Over the Weekend, please hit the heart button at the bottom of this message and share this post with others!

Disclaimer: The “Antagonist Stocks and Options Research” newsletter (hereafter: The Antagonist) is an online financial literacy resource. All materials from The Antagonist are intended for informational and educational purposes only. They are not, nor are they intended to be, trading or investment advice or a recommendation that any security, futures contract, transaction or investment strategy is suitable for any person.

By subscribing to this newsletter, you acknowledge that you understand and agree to these terms and conditions. Read the full disclaimer here.